a case of mirror and smoke?")

January 04, 2024 (MLN): The attraction of quick gains in a bullish market often blinds investors to the deeper currents underneath the surface. Such could be the scenario witnessed in the PSX during this bullish trend, where shareholders with major holdings benefit from surging stock prices, while minority investors are attracted to cases like Treet Battery Limited (TBL) despite its limited free float.

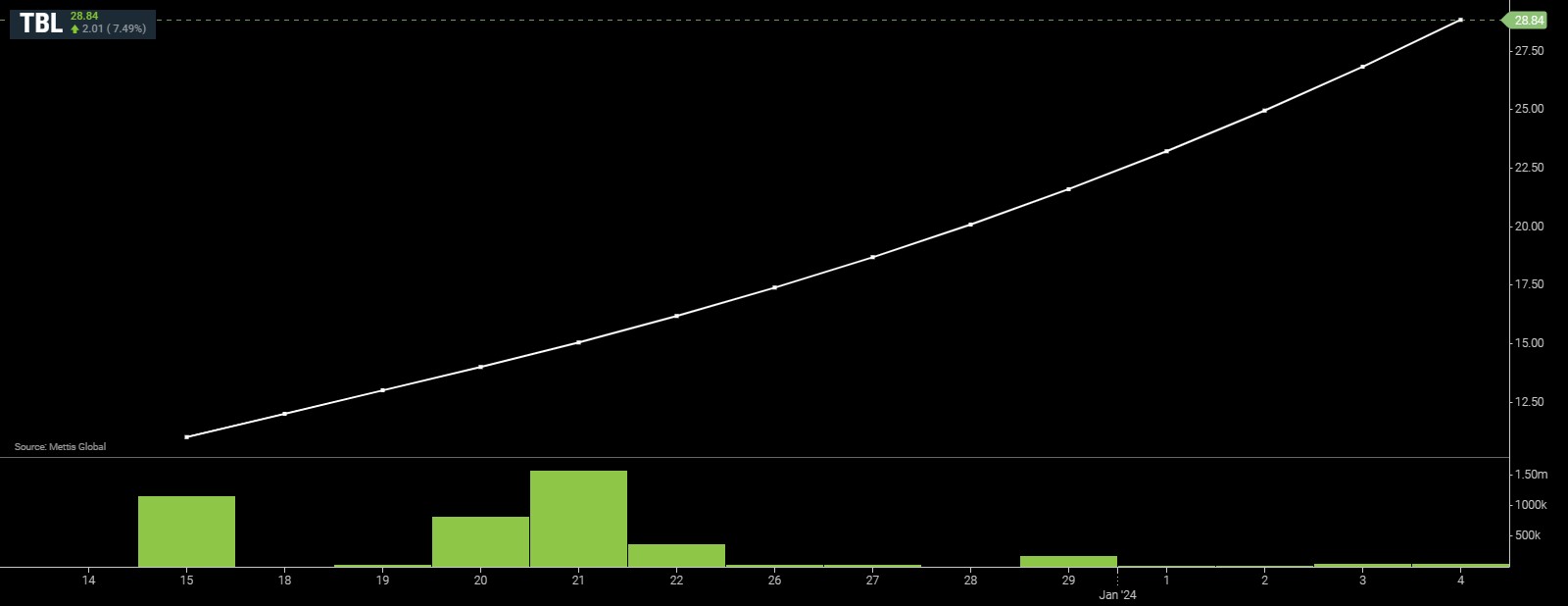

TBL made its debut on the PSX on December 15, 2023, at Rs10 per share. As of January 04, 2024, within just 14 trading sessions, the stock has surged to Rs28.84, marking an astounding 188.4% increase or a 2.88x rise in value.

Upon investigation, it has surfaced that the investors possibly lacking sufficient scrutiny, are drawing comparisons between TBL and other battery companies. They anticipate TBL's share price to surpass the other companies, without adequately considering the substantial differences in their financial performances.

Moreover, a comparative analysis portrays that TBL is substantially overvalued compared to other listed battery companies.

| TBL | EXIDE | ATBA | |

|---|---|---|---|

| Price (January 04, 2024) | 28.84 | 387.2 | 241 |

| Book Value per share | 1.49 | 656.52 | 207.11 |

| Price to book value | 19.42 | 0.59 | 1.16 |

| Price to earnings | -108.74 | 3.99 | 3.83 |

| Price to sales | 3.08 | 0.13 | 0.20 |

| Note* Sales/Earning are annual, respective to the individual company's year-end date | |||

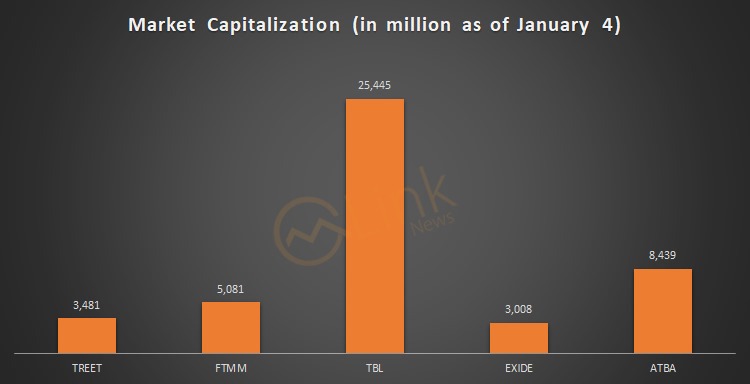

Market cap of TBL left everyone behind:

Following the dramatic rise of TBL’s stock price, its market capitalization surpassed that of its parent company, TREET, within just fourteen trading sessions.

As of its debut on December 15, 2023, at an initial market capitalization of Rs8.8bn, TBL marked an unprecedented surge of 188.4% within a short period to reach Rs25.44bn in market cap at the time of writing.

This rapid escalation, coupled with TREET’s overwhelming dominance and control, prompts questions about potential vulnerabilities in TBL's stock price. The anxiety of major shareholders can be sensed as the price has reached a point where any substantial sell-off could precipitate a significant drop in TBL’s stock price.

The disproportionate control exerted by TREET over TBL raises concerns about potential market manipulation practices like "pump and dump." Such circumstances warrant a closer examination to ensure fair and transparent market dynamics, safeguarding investors' interests.

Such actions could leave the shareholder of a mere 5%, 3% or 1% free float helpless to the whims of the dominant parent company.

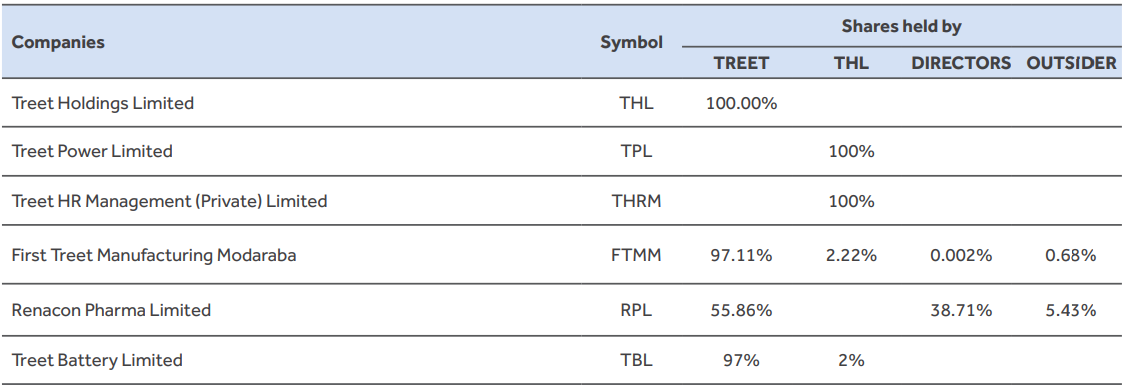

TBL’s free float is 5%, 3% or 1%?

The free float of TBL is a grand guessing game as the PSX website shows a 5% free float, implying the remaining 95% is held by TREET, the parent company. However, the annual report contradicts this, asserting that TREET holds 97% of TBL while THL holds 2% of TBL which means the free float is only 1%.

This remains a mystery why the concerned department at PSX hasn't noticed this difference in free float.

Source: Annual Report 2023

No impact on TREET price:

Despite TREET holding a substantial 97% share in TBL and reaping considerable gains from its surging price, it's puzzling to witness TREET's stock price stagnating around Rs19, especially when it was expected to rise. Logically, with TREET being the major shareholder of TBL and having a 45% free float, shareholders of TREET should benefit from TBL’s surge. However, the staggering price behaviour of TREET indicated that something fishy might be happening.

What is the motivation behind this demerger from FTMM?

The decision by FTMM to demerge TBL, a company that operated under FTMM for years, triggers inquiry. It's important to discern what prompted this change, considering that TBL is an established entity.

Upon delving into the scheme of the merger document, it's apparent that the principal objective is the segregation of specific assets and businesses of FTMM, alongside their respective liabilities and share premiums, transferring them to TBL.

The stated benefits of this scheme include de-bundling business units for value exploration, accessing international markets, additional fund-raising opportunities, value creation for Modaraba Certificate Holders, and providing voting rights for existing holders.

However, closer scrutiny of the company's financials reveals that the battery segment of FTMM has incurred losses over the past few years.

For further investigation, we approached the company's official who revealed that FTMM, being a Shariah Compliant Modaraba entity, was no longer able to conveniently finance TBL.

This situation forced them to demerge TBL from FTMM so that they could arrange conventional financing for TBL.

| FTMM (Battery Segment) | |

|---|---|

| Operating Profit/(Loss) | |

| 2023 | 255.1 |

| 2022 | (296.6) |

| 2021 | (660.8) |

| 2020 | (1,508.8) |

| 2019 | (2,178.6) |

| 2018 | (353.9) |

| Amount in PKR Million | |

The company in its annual report conveniently attributed the losses of the battery division to an escalation in financial charges, driven by domestic economic challenges.

“The battery segment achieved its first-ever operating profit of Rs610 million in 2023, a substantial improvement over the Rs274 million loss incurred in the same period last year. It is important to acknowledge that the escalation in financial charges, driven by domestic economic challenges, has led to a significant increase in financial expenditures. Consequently, the segment recorded a net loss of Rs234 million. It is worth noting that this loss is considerably less when compared to the corresponding period in the prior year (Net Loss 2022: Rs771 million),” according to the company’s annual report.

The aforementioned finding raises brows that listing TBL as a separate entity might aim at shedding a loss-making venture, transferring associated liabilities amounting to over Rs8bn. This raises concerns about the underlying motives behind this demerger, particularly considering the financial obligations inherited by TBL.

| TBL Balance Sheet | |

| Non-Current Assets | 7,576 |

| Current Assets | 1,748 |

| Total Assets | 9,325 |

| Non-current liabilities | 156 |

| Current liabilities | 7,858 |

| Total liabilities | 8,014 |

| Net Assets | 1,311 |

| Amount in PKR Million | |

Scrip price cap unquestioned:

Today was the fourteenth session and during all sessions, the scrip price was capped but lo and behold, the concerned department at PSX seems to be on a break from asking the company about this peculiar and consistent occurrence.

Pakistan stock exchange should establish and implement a protocol to investigate unusual share movements, triggering inquiries after a certain percentage increase or decrease in prices. This mechanism should be strictly applied to both upward and downward price fluctuations.

Call for regulatory reforms to ensure market fairness and transparency:

Where there's smoke, there's fire. The aforementioned facts and concerns vividly illustrate the pressing need for strict vigilance and regulatory scrutiny.

The puzzling interplay between soaring stock prices and the contradictory free-float shares portrays a picture of potential manipulation within the investing community.

This situation not only risks market integrity and fairness but also poses questions about the due diligence and oversight exercised by the Pakistan Stock Exchange (PSX) in admitting companies where a leading parent entity holds sway.

Upon inquiry, we discovered that there is no minimum limit set for technical listing companies to restrict the free float. Consequently, TBL's free float stands at 1%.

On the contrary, clear guidelines exist for determining the minimum free float of companies listed due to reverse mergers.

The listing committee of PSX should also establish a minimum limit for free float applicable to technical listing companies as the listings with significantly low shares held by minority shareholders create an environment conducive to pump-and-dump schemes.

Furthermore, the free float should be adequate to facilitate public trading. If a company lacks sufficient float for trading, all transactions should be deemed null and void.

Removing listing loopholes is crucial to safeguard the interests of minority shareholders.

Background:

TBL entered the Exchange following the de-merger and bifurcation of the Battery Division of First Treet Manufacturing Modaraba (FTMM), a listed Modaraba, via a Scheme of Arrangement sanctioned by the Lahore High Court through an Order dated January 10, 2023.

According to the company’s financials, the management has allocated Rs8bn in 2023 to TBL in terms of investments which was previously added under the head of FTMM.

According to the disclosed swap ratio in the Scheme, certificate holders of FTMM received 0.9984 shares of TBL for every 1 certificate of FTMM.

The scrip settlement occurred on a T+2 basis, with the first settlement date being Tuesday, December 19, 2023. TBL is categorized under the "Automobile Parts & Accessories" sector in the daily quotation of the exchange.

The Lahore High Court (LHC) has sanctioned the Scheme of Arrangement for the de-merger of the battery division and the consequent transfer of all assets and liabilities of the battery division from First Treet Manufacturing Modaraba (FTMM) to Treet Battery Limited, the company filing on PSX revealed on Wednesday.

To recall, on January 24, 2022, the management of FTMM filed a petition before LHC for the demerger of the battery division.

This is a reference to the approval accorded by the board of directors of the management company, fulfilment of all legal and regulatory requirements and under the relevant sections of the Companies Act, 2017.

Copyright Mettis Link News

Posted on:2024-01-04T16:47:01+05:00

42491