July 27, 2022 (MLN): Pakistan’s Eurobonds continue to take a beating and have come under further pressure in July, despite the government managing to sign a Staff Level Agreement (SLA) with the IMF that will result in the release of a $1.2 billion tranche in August under the Extended Fund Facility (EFF).

The expectation was that Pakistan’s credit spreads will start to narrow once the IMF review is approved, as it will release pressure on the country’s foreign exchange reserves and also pave the way for other sources of bilateral and multilateral funding. Even Moody’s termed the decision as “Credit Positive”.

However, the reality turned out to be harshly different with the spreads on Pakistan’s Eurobonds significantly underperforming that of its peers such as Egypt and Nigeria. The current spread reflects a heightened risk of default with the curve still inverted.

While I fully subscribe to the notion that “Spreads Don’t Lie”, I believe there are times when “Spreads Do Magnify” the actual credit risk. Before taking a deep dive into Pakistan’s prospects of avoiding default or otherwise, it will be helpful to review the performance of EM credit, in general, this year. This will provide a meaningful context to the malaise that Pakistan’s Eurobonds face currently.

2022 is turning out to be an annus horribilis for EM credit, with H1 2022 return of over minus 20% as measured by JPM EMBI Global Diversified Index. The asset class remains under a cloud driven by multiple factors including rising US treasury yields, geo-political tensions, volatile commodity prices, rising inflation, and capital outflows.

EM credit faces several headwinds for the rest of the year with Fed’s front-loaded tightening plans through faster rate hikes and balance sheet reduction picking pace from September, continued geo-political tensions, and increasing domestic political and social challenges. EM economies, especially the energy and food importers are facing widening current account and fiscal deficits, massive inflationary pressures, and sharp currency weakness. Some of the worst affected credits in the EM sell-off are Egypt, Ghana, Nigeria, Pakistan, and Turkey, to name a few.

Within EM credit, there is a significant divergence in performance with GCC credit outperforming and HY bonds have suffered the most. Within the HY segment, the performance of credits rated below BB is the worst. The spread on single B-rated credits (part of JPM EMBI Global Diversified Index) stood at 873 bps as of 30th June – change of 270 bps during the 2nd quarter and a YTD change of 230 bps.

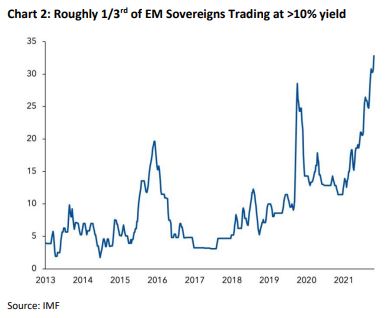

Spreads on junk rated EM sovereigns started to widen from mid-February as the conflict between Russia and Ukraine escalated and then turned into a full-scale war. The widening picked up pace in March and after a brief respite in May, resumed in June and has continued since then. As of end-June, yields on the external debt of around 1/3rd of EM sovereigns (a total of 18) were trading above 10% – a level that is considered “Distressed”. The situation is especially grave for EM economies that rely on external financing as tightening financial conditions and rising borrowing costs are shutting out such sovereigns from accessing debt markets. That’s why we have seen an increasing rush to the IMF for support from countries such as Egypt, Ghana, Pakistan, Tunisia, Bangladesh, and Sri Lanka (after defaulting in April on its external sovereign debt).

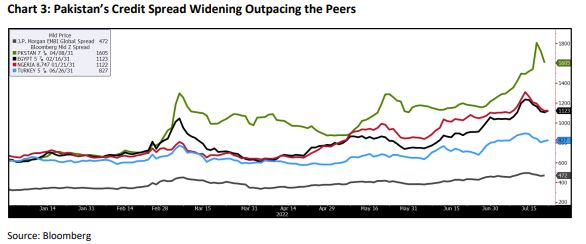

Comparing the spread movement on Pakistan’s Eurobonds with similar rated peers such as Egypt, Nigeria and now Turkey (post the recent downgrade by Fitch) does not paint a pretty picture. After trading at a very narrow differential to both Nigeria and Egypt in mid-May, the spread on Pakistan 2031 Eurobond has widened considerably and currently trades around 500 bps higher than that on Egypt 2031 and Nigeria 2031 bonds.

The situation for Pakistan has worsened further over the last two weeks driven partially by worsening economic indicators, and mostly due to the continued political and governance turmoil that the country is going through since the change in government in April. The political upheaval at the Center and now in Punjab, the biggest province is causing uncertainty among investors at a time when there is a very limited risk appetite for junk bonds.

According to JP Morgan, Pakistan with a negative 40.3% YTD total return is the fourth worst performer in the EMBIGD after Ukraine (-72.8%), Sri Lanka (-45.4%), and Argentina (-41.9%). The recent sell-off is even more worrying as EMBIGD HY is up 5.1% since 14 July whereas EMBIGD PKSTAN is down 6.9% in the same period.

The Question – Why So Distressed?

Is there solely an economic justification to such elevated spreads? The answer is No, and here is why. The agreement with the IMF will unlock additional funding from other multilateral and bilateral partners. The IMF board is also likely to approve an extension in the EFF until June 2023 and increase the size by another USD 1 billion. This will help the country in meeting its higher financing needs during FY2023 (July 2022-June 2023).

The key risk is the implementation of the program conditions by the political government given the current scenario and Moody’s summed up the development in following words: “We expect the IMF Executive Board to approve the USD1.2 billion disbursement in the third quarter of this year. We also expect Pakistan to maintain its engagement with the IMF, which would catalyse financing from other external sources as it focuses on policy priorities that the IMF has identified, including implementing the fiscal 2023 budget, making progress on power sector reforms, lowering inflation, reducing poverty, enhancing governance and mitigating corruption. In this scenario, we expect Pakistan to be able to meet its external financing needs for the next few years. Nonetheless, Pakistan’s ability to complete the current EFF programme and maintain a credible policy path that supports further financing remains highly uncertain, while elevated inflation and a higher cost of living are adding to social and political risks. The government may also find it difficult to continually enact revenue-raising reforms, such as steadily increasing petroleum levies and raising power tariffs, particularly in the run-up to the next general elections scheduled for mid-2023.”

Fitch, that recently downgraded the outlook on Pakistan to Negative also highlighted the political risk as a key reason for the change.

“Renewed political volatility cannot be excluded and could undermine the authorities' fiscal and external adjustment, as happened in early 2022 and 2018, particularly in the current environment of slowing growth and high inflation. The new government is supported by a disparate coalition of parties with only a slim majority in parliament. Regular elections are due in October 2023, creating the risk of policy slippage after the conclusion of the IMF programme. External funding conditions and liquidity will likely improve with the new staff-level agreement. Nevertheless, slippage against programme conditions is a risk and could quickly lead to renewed strains, while diminished FX reserves and high funding needs now leave less room for error. Pakistan's access to market finance could remain constrained.”

Let’s look at some of the “positives” first. Pakistan’s external funding needs (CAD + Short term external debt) for FY2023 are likely to be fully covered through (a) the release of IMF tranche in August; (b) extension in the EFF until June 2023 and an increase in size by USD1 billion; (c) rollover of bilateral deposits kept at the central bank, and extension in oil credit facility from Saudi Arabia; (d) additional inflows from multilaterals such as the World Bank, ADB; and (e) collateralized borrowing from a gulf country using shares of public sector enterprises.

This was confirmed recently by the Acting SBP Governor in a podcast and supported by both Moody’s and Fitch. Both Current Account and Fiscal deficits are projected to narrow in the current fiscal year. Similarly, Pakistan has to repay only USD1 billion of sukuk maturing in December 2022. This places Pakistan at a relatively similar or better position when compared to countries such as Egypt and Turkey.

Similarly, comparing debt indicators such as total debt/GDP ratio and gross financing requirements/GDP indicate that Pakistan’s credit spread is disproportionately wider compared to that on peers.

The irony is that there are two key indicators that are moving in the wrong direction, clouding the positives. First is the PKR/Dollar rate that has sunk to new lows this year. On a YTD basis Pak Rupee is down over 24% vs. the USD and is the second worst performer globally after Turkish Lira.

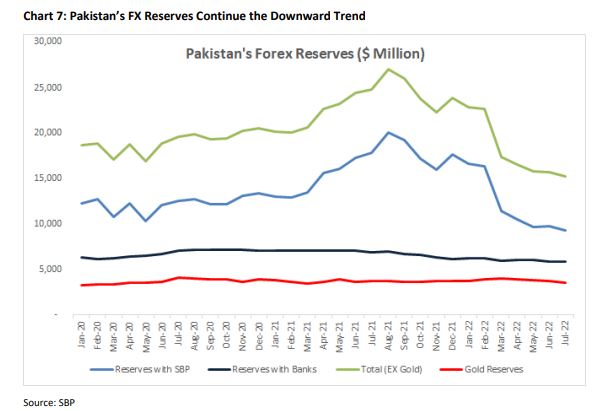

The central bank has mostly stayed on the sidelines and this has led to panic and a sustained weakness in PKR in the domestic market. Second, Pakistan’s foreign exchange reserves (held by the SBP) have continued to bleed in 2022, and as of July 15 stood at USD9.3 billion – providing less than 2 months of import cover and reflect a fall of USD8.3 billion from the start of the year. However, it is encouraging to note that reserves held with commercial banks have stayed stable at around USD6 billion during the same period. Furthermore, the SBP holds gold of around 2.08 million troy ounces, with value of USD3.5 billion (at current price).

As per the SBP podcast, if required, these gold reserves can be used to raise liquidity. This provides a significant liquidity backstop in the event there is any potential shortfall in the external funding needs for the year.

Bridging the Gap

It is evident that political uncertainty and the resulting policy paralysis are causing upward pressure (justifiably) on credit spreads. The current government first procrastinated in taking tough decisions that were critical to secure the IMF funding. After those steps were taken and the SLA was signed with the IMF, the immediate reaction was seen in the by-elections in Punjab where the ruling party was trounced by Imran Khan led PTI. Emboldened by the victory Mr. Khan immediately increased pressure on the government and gave a call for early elections.

“The only way forward from here is to hold fair & free elections. Any other path will only lead to greater political uncertainty & further economic chaos.”

This has raised concerns that political instability and the risk of erosion of political capital due to tough economic measures will make the government reluctant in taking steps required for a successful implementation of the IMF program. The coalition government faces a political dilemma – go ahead with the implementation of conditions, losing political capital and pay the price at the next general elections Or resort to populist policies leading to slippage on key targets and risk suspension of the program before completion, and push the country to the brink of a sovereign default. I believe either of these scenarios are unacceptable to the ruling coalition as the outcome is an election defeat (lose-lose situation).

Therefore, the coalition government once again faces a tough decision. After securing the IMF board approval for the next tranche and completing bilateral funding agreements with “friends” in the GCC, the government should announce fresh elections and hand over power to a caretaker technocrat government.

The risk of slippage in implementation under a caretaker government will be markedly lower and will help in reducing the credit spreads from current elevated levels. I understand that this decision requires a great degree of political maturity and economic acumen, both of which are lacking in the ruling coalition. However, given the evolving situation, if they don’t decide this voluntarily, they will be forced to do the same.

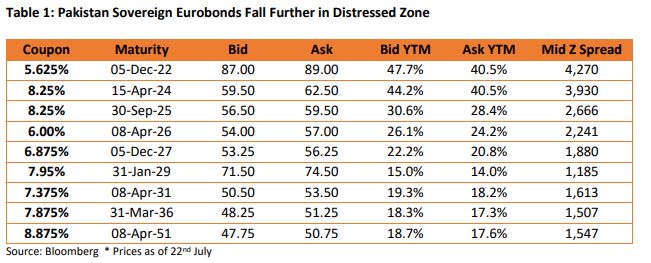

What are my recommendations on Pakistan’s Eurobonds now? Pakistan sukuk that matures on 5th December this year will be repaid in full. It is currently trading at a price of 90 (yield of ~ 37%). This one is a clear Buy for me. The bonds in the belly of the curve (2024-2027) trade at mid-50s to low-60s.

Assuming a scenario where Pakistan needs a debt restructuring/reprofiling in 2023 or 2024 (not ruling this scenario out completely), these bonds will get hit further. Hence, I am avoiding the belly as of now. Pakistan 29 sukuk is the least attractive on the curve in terms of risk/return trade off.

This will probably find buyers after the repayment of 2022 sukuk. Pakistan 31 and 51 are trading around cash price of 50. This is very close to the recovery value as well. Hence, I recommend a Buy on both Pakistan 2031 and Pakistan 2051.

My last recommendation is a Buy on Pakistan WAPDA green bond maturing in June 2031. The bond is trading at a cash price of ~ 47 and yields over 21%. Being the largest electricity producer, WAPDA is a strategic entity and will remain a key player in the power sector of the country.

By Mohammad Ahsan

Managing Director, Rates and Fixed Income at Mashreq Bank

Please note that these are the author’s personal views and do not reflect the view of Mashreq Bank.

34292