September 30, 2021 (MLN): Fitch Solutions has revised weaker its forecast for the Pakistani rupee to average PKR164.00/USD in 2021 and PKR180.00/USD in 2022, from PKR158.00/USD and PKR165.00/US previously.

In its latest report, Fitch Solutions said that the expectation for the currency to weaken further is based on Pakistan’s worsening terms of trade, tighter US monetary policy, alongside the flow of USD out of Pakistan and into Afghanistan.

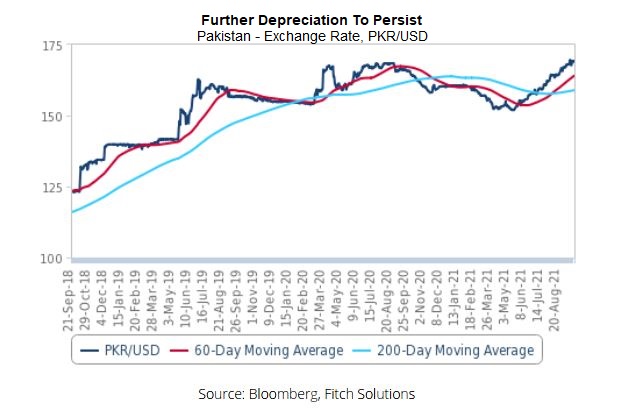

Since its last update in June 2021, PKR has depreciated by 7.1% to PKR169.31/USD and the rupee has averaged PKR159.23/USD over the first nine months of 2021. The sell-off can largely be attributed to the country’s increasing import bills, alongside external factors stemming from neighbouring Afghanistan.

Moving forward, it is expected these factors to continue exerting a depreciatory pressure on the rupee. As such Fitch has revised its forecast for the Pakistani rupee to average PKR164.00/USD in 2021.

From a technical perspective, the report sees scope for further depreciation of the rupee against the US dollar. The unit continues to be above both long and short-term moving averages, suggesting a deprecatory trend over the medium term.

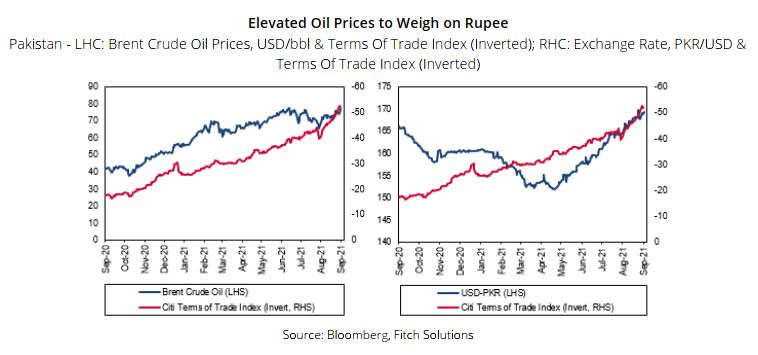

From a fundamental perspective, it is expected that the currency would weaken due to worsening terms of trade on the back of higher oil prices. On average, the country’s trade deficit has been widened on a year-on-year basis this year coming in at -USD2.9bn vs -USD1.7bn across the same period in 2020.

This comes as oil prices averaged USD67.68/bbl year-to-date compared to USD43.20/bbl in 2020. Going by the report, it is expected this trend of strong oil prices to persist as the Fitch Commodities team forecasts Brent crude oil prices to average USD70.00/bbl in 2021. With oil accounting for a large share of Pakistan imports (20.1% of total imports), an increase in oil prices over 2021 will worsen Pakistan’s terms of trade, thereby weighing on the PKR over the coming months.

Meanwhile, it is not expected the State Bank of Pakistan’s (SBP) monetary tightening cycle over the coming months to be sufficient in offsetting the strengthening pressures on the US dollar.

The Federal Reserve has signalled its intention to begin tapering asset purchases over the coming months due to progress made on the improvement of the US labour market as well as growing inflationary pressures domestically. The expectations for a hawkish shift by the Federal Open Market Committee (FOMC), will likely put upside risks to US dollar strength over the coming months.

While the SBP will also be tightening monetary policy, the research forecasts 100bps of hikes to the policy interest rate by June 2022 – persistently high risks regarding the country’s assets due to Pakistan’s twin deficit status inform Fitch’s view that this will fall short in offsetting the rupee’s depreciation against the USD.

The report further highlighted that the greater transfer of USD from Pakistan to Afghanistan will also weigh on the Pakistani rupee. According to Pakistani Media house, approximately 25% of USD supply in the Pakistani banking system has been channelled across the border. As such, the increased demand for the USD will mean weakness in the PKR/USD unit.

With regards to Long-Term Outlook (six-to-24 months), the report noted that the higher structural inflation as compared to the US will weigh on the rupee. It is forecasted that inflation in Pakistan to average 7.6% between FY22 and FY23, well above its average forecast of 3.3% over 2022-23 for the United States.

Higher inflation will erode the competitiveness of Pakistan goods in the international market and will require depreciation of the currency to preserve the competitiveness of Pakistani exports, it added.

Meanwhile, although Pakistan is likely to grow by 4.5% on average between FY22 and FY23, outpacing that of the US at 2.8% over 2022-23, a poor business environment is likely to continue deterring foreign businesses from investing in Pakistan and this will limit the support economic growth can have on the rupee’s strength.

Indeed, Fitch operational risk index for Pakistan comes in at 41.8 out of 100, lower than 77.9 for the US, indicating a sharply weaker business environment.

That said, the CPI-weighted real exchange rate (REER) of Pakistan is currently trading 2.7% below its 10-year average amid the recent sell-off, suggesting that the unit is undervalued. The report expects the real undervaluation of the rupee to limit excessive weakness in the currency over the longer term as a weaker currency should improve the competitiveness of exports while simultaneously making imports relatively more expensive, providing some support to the PKR/USD.

Risks To Outlook

Risks to Fitch Solution currency outlook are weighted towards the downside. Fitch currency forecast accounts for Pakistan to continue to receive the IMF Extended Facility Fund which would allow for the disbursement of a loan tranche worth approximately USD1bn. Talks have been stalled since June following disagreements surrounding IMF recommendations on further hikes in energy tariffs alongside higher personal income tax and GST reforms. Renewed negotiations are expected to be held on October 4.

The report suggests that further delay or even an abandonment of the IMF programme would dampen investor’s sentiments, leading to an outflow of capital and a worse sell-off in the PKR than it currently expects.

Copyright Mettis Link News

27161